Could Derivatives Trigger a Financial Crisis?

The Dow Jones Industrial Average has crossed above 41,000, the S&P 500 is making a run towards 6,000, the Nasdaq Composite Index stands at 18,000. Everything feels great. But be very careful: a financial crisis is still possible—and it wouldn’t be wrong to say the odds are increasing.

There’s one thing that’s really worth keeping a close watch on these days: derivatives.

Derivatives 101: They are essentially contracts between two parties based on the value of underlying assets. They are used for many purposes, such as hedging, speculating, or just getting access to difficult assets or markets.

You see, derivatives are not discussed much in the mainstream, but they have the ability to cause a financial crisis very quickly. Just so you know, the last crisis, which we saw back in 2008–2009, was triggered by derivatives based on the housing market.

Massive Amount of Interest Rate Derivatives

Now let’s dig into the details…

In the first quarter of 2024, combined, all U.S. banks had derivatives with a notional value of $206.1 trillion and had total assets of $21.42 trillion. (Source: “Quarterly Report on Bank Trading and Derivatives Activities: First Quarter 2024,” Office of the Comptroller of the Currency, last accessed July 17, 2024.)

So, for every dollar of assets, U.S. banks have derivatives with a notional worth of about $9.62.

The troubling part is that the vast majority of these derivatives are concentrated around interest rate products—about $144.4 trillion, or 70.1% of total derivative notional amounts!

An Inflection Point in the Interest-Rate Cycle

Why is it troubling to have so many derivatives based on interest rates?

No rocket science here really, but it is important to understand that we at an inflection point when it comes to the interest rate cycle.

The Federal Reserve was trying fight inflation for a while; in order to do so, it raised interest rates very quickly. Now the Fed is hinting that rates could be coming down this year and the next.

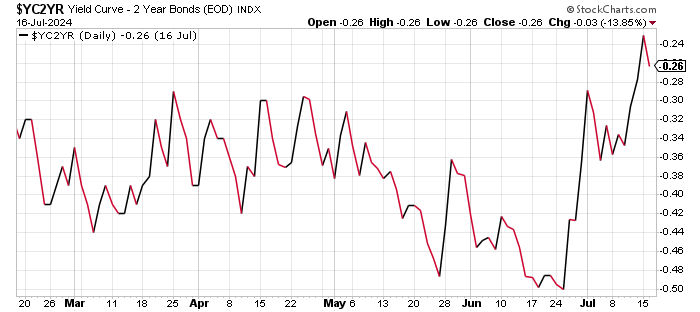

As all this happens, the yield curve is starting to steepen a bit after being in deep inverted territory for a very long time. You can see the chart below to get some perspective on how it’s looking.

Chart Courtesy of StockCharts.com

Since near the end of June 2024, the yield curve has steepened close to 25 basis points, and it looks like it could be changing direction. Essentially, this is hinting that investors could be anticipating interest rate changes as well.

Overall, though, the interest rate market knows that rate cuts are coming, but there’s a lot of uncertainty on how low they could last and the timing of it is extremely questionable.

Why a Financial Crisis Shouldn’t Be Ruled Out Just Yet

So, what’s really the problem?

Dear reader, I can’t stress this enough: don’t take derivatives lightly, especially with the yield curve steepening and so much uncertainty around what will happen to interest rates going forward.

It’s important to understand that, with derivatives, things can go from good to bad to ugly very quickly. Don’t just look at the financial crisis of 2008–2009. There have many several examples in the recent past where derivates going bad caused major losses for banks.

Just imagine this: there’s $144.4 trillion in notional derivates—and assuming 10%–15% of these derivatives are held by banks that are on the wrong side of the trade—and we get some sort of shock in the financial markets that progresses the interest rate trajectory faster than predicted.

What happens then?

What if the trajectory of interest rates changes completely, and we started talking about raising rates again?

I think that even a small percentage of interest rate derivatives going bad could be detrimental—it could take a few banks with it. When that happens, you get a financial crisis. And it’s never a pretty sight…all assets feel the impact.