Would the Political Tensions Facing Trump Weaken the U.S. Dollar?

The various scandals that have been distressing President Donald Trump over the past months are about to spill over to the financial markets. Wall Street won’t be the only one affected; all major stock exchanges will get the ripple effects. But one of the surprises will also be the course of the U.S. dollar in 2017.

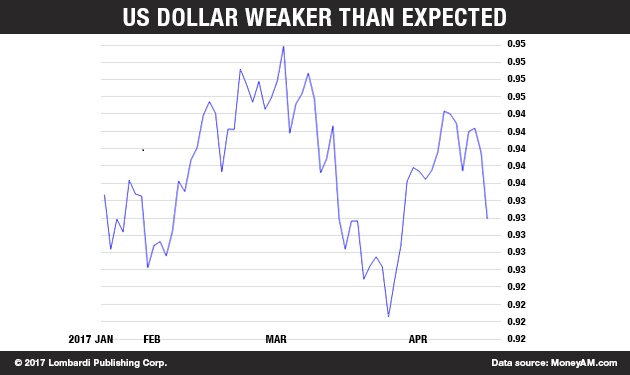

Trump was concerned that the dollar would go so high compared to major currencies that it would hurt American industry. Instead, it seems Trump has to worry about the opposite problem: is the U.S. dollar weak? If any more proof is needed, the gold price momentum is higher, having climbed for several consecutive sessions in a row as the Trump-Washington establishment feud thickens.

Advertisement

Investors are increasingly worried by the rumors of impeachment against President Trump. This event is no longer just in the realm of possibility; a Trump impeachment has become a probability. The gold price trend has gone decidedly bullish compared to the start of 2017. The rising price of gold, meanwhile, is a direct effect of a U.S. dollar forecast for 2017 that has turned from overly bullish to bearish.

The downside risks to the dollar go even beyond Trump’s political fortunes. The U.S. economic outlook itself is far less optimistic than the stock markets’ performance so far in 2017 would suggest. In the short and medium term, Trump’s troubles with Congress, the specter of a protracted investigation that will distract the White House, and North Korean threats certainly raise the question: will the U.S. dollar collapse?

Indeed, apart from the pure market perception, the judicial problems that are shaping up for President Trump will weaken his resolve to engage. His attention will move to personal legal battles instead of those that America and Americans need someone to fight for them. Whatever happens on Wall Street is contagious. When the signal is toxic, the bearish sentiment spreads globally and quickly.

The market tension is high all over the world. The Asian stock markets have reacted bearishly to the allegations against Trump. The Nikkei index in Tokyo lost more than half a percentage point, as did the Sidney stock exchange in the week ending on May 19. The Japanese yen and the euro, in turn, gained against the dollar, heading towards values not seen since the day after the U.S. election.

A more stable political climate in the United States would have brought the dollar and euro to parity by now. Instead, a day does not pass without new fiery revelations against Trump. Thus, the dollar is being hammered. The turmoil has also put pressure against Wall Street and the stock exchanges around the world.

Just weeks ago, if anyone had asked: Is the Trump bubble going to burst? The most pessimistic answer might have been: Probably. But as of now, Trump’s name has become ever more associated with “Russiagate” than “economic growth” or a high U.S. dollar.

Trump Faces Too Many Obstacles

Still, Trump had many elements stacked against him. The establishment was never going to allow President Trump to pursue his agenda. Trump has faced obstacles immediately after winning the elections. There were protest marches—worldwide no less—on the very weekend after Trump took the Oath of Office on January 20. The new president barely had time to put his pen on the Oval Office desk before the world was already challenging him in the streets.

Still, nobody could have expected a U.S. dollar collapse in 2017. That seemed unthinkable. The Federal Reserve Chair, Janet Yellen, confirmed her commitment to raising nominal interest rates. They would go back up to at least one percent before the end of the year. Instead, a poor GDP performance has stopped the rate increases. But nobody had foreseen how quickly Trump’s problems could affect the American currency.

It all happened in the span of a few weeks. President Trump decided to dismiss FBI director, James Comey. The mainstream media took that move and had a party with it. They drummed up ghosts of President Richard Nixon and the so-called “Saturday Night Massacre.” It didn’t take long for the word “Watergate” to appear. True or false, justified or unfair, the term Watergate has all but created a constitutional crisis in the United States. That cannot be good for the U.S. dollar.

But that’s not all. The Washington Post revealed that Trump—whose staff was already in the Washington political establishment’s viewfinder over relations with Russia—allegedly leaked intelligence to the Russians. (Source: “Trump revealed highly classified information to Russian foreign minister and ambassador,” The Washington Post, May 15, 2017.)

Now, the information concerns ISIS and the potential threats it might pose to civilian airliners. It doesn’t sound all that unreasonable for Trump to share that information, considering that ISIS is a mutual enemy of the U.S. and Russia. But Trump is no ordinary president. Washington, Republicans and Democrats alike, have been waiting, and wanting, for Trump to slip up.

Add that to the alleged memo that Comey wrote, noting that Trump had asked him to drop the investigation into former national security advisor Michael Flynn and there’s no escaping the fact that Washington will be in turmoil in 2017. That will doubtless affect Wall Street and the U.S. dollar in a significant manner. Trump is now being chased by the shadows of Nixon and Clinton and the charges of obstruction of justice. It might be too early to speak of a U.S. dollar devaluation or a U.S. dollar collapse. But, the U.S. economy will have to deal with a much weaker dollar than expected.

The Economic Consequences of a Weak Dollar

Political troubles aside, President Trump had abandoned the traditional strong dollar presidential policy. If anything, he had expressed concerns that the high dollar was creating unwanted effects. A strong dollar might be “prestigious” and certainly gives the impression of “Making America Great Again.” Yet, it also weighs heavily against U.S. business.

Therefore, there is a silver lining to Trump’s political problems. Inadvertently, and no doubt reluctantly, Trump has found a way to balance the Federal Reserve’s tightening monetary policy with what seemed like an unstoppable rise of the dollar. The weaker dollar should also make it easier for Trump to push American exports, especially as he prepares to meet the leaders of the world’s seven richest countries—the G7.

Trump has consistently said that U.S. companies have been disadvantaged by past trade agreements. He has been threatening to impose tariffs against a number of European imports and altering sections of the North American Trade Agreement (NAFTA) as well as scrapping membership in the Trans Pacific Partnership (TPP) altogether. That was one of President Obama’s biggest foreign policy pursuits.

Trump is right. Exchange rate is a key driver of business flexibility and import appeal. However, the president’s margin of influence on the dollar is limited. The dollar outlook is generally determined by a broad spectrum of factors. Still, the overall logic supports Trump’s desire to reverse the dollar’s strength. Trump’s fast rising mountain of political problems have been rather punctual in that regard.

The U.S. dollar has gone simply too high. There can be no doubt about that. The Greenback has appreciated well over 20% since July 2014. This puts U.S. companies under pressure when they compete on international markets. Exports remained stable until around 2014, when they began to deteriorate and weigh on the economy. In February of 2016, U.S. exports showed a historic decline. (Source: “U.S. exports drop for first time since Great Recession,” CNN Money, February 5, 2016.)

The context of the exports decline is what makes this a critical problem. The world economy is suffering, even more than the American one. Thus, the high dollar makes it all the more difficult for American companies to compete in such a climate. The world economy, particularly Europe, has not shown any especially optimistic economic results lately.

The European Central Bank (ECB) did boast that the recession is over. But it hasn’t yet changed its zero interest rate policy. That suggests two things. 1. European appetite for American cars and other goods won’t increase any time soon. 2. The exchange rate between the dollar and the euro won’t change in the direction that American exporters want.

Now, Trump’s Russiagate has created that opportunity. The rapid appreciation of the dollar, rather, has penalized growth. Trump now does have a chance to boost American GDP. Had the dollar continued its climb unhindered, it would have accentuated the deterioration in the trade balance. Now, the big question will be as hinted earlier, just how willing the Fed might be to raise interest rates. Currencies tend to move ahead of rates as investors revise their expectations in response to the overall market. The climate now is pessimistic and the dollar has started to fall all on its own. This means that Janet Yellen could still entertain rate hikes.

But, the fallout from Trump’s political problems is still unclear. The markets could crash and spark another recession. Thus, nothing is clear. That kind of uncertainty will put even more pressure on the dollar.

The United States economy, meanwhile, has not shown any sign of reversing the course of its growing public debt, which has exceeded 100% of GDP. The private debt situation is even more of a concern. The dollar amount of derivatives and other toxic financial instruments, indecently called “investments,” far exceeds $1.0 trillion.

The bulk of this virtual money is denominated in U.S. dollars—dollars fully secured by the U.S. Treasury, and by it alone. Washington, however, is unable to balance its budgets, and Trump’s tax plan does little to avoid a further increase in debt. The dollar has many obstacles stacked against its rise and a collapse is inevitable.