With the Next Recession Looming, Central Banks Will Enact Negative Rates to Avoid a Devastating Crash

Just when you thought the monetary insanity couldn’t get any crazier, think again. Negative rates might be commonplace in the next couple years, in an effort to keep American consumers and businesses solvent. This is the natural evolution, over-indebtedness, that knows no bounds.

The latest idiocy comes via Bloomberg Markets, where they opine in their lead paragraph that “central banks will need to be prepared to cut interest rates deep into negative territory in the next economic downturn.” (Source: “With Next Recession Looming, Central Banks Better Make Peace With Negative Rates,” Bloomberg Markets, August 14, 2017.)

Advertisement

Bloomberg references a new paper by Harvard professor Kenneth Rogoff in the Journal of Economic Perspectives. In it, Rogoff argues in favor of negative rates, prodding policymakers to develop market infrastructure before the next downturn arrives. “It is time for economists to stop pretending that implementing effective negative rates is as difficult today as it seemed in Keynes’s time,” Rogoff writes. (Source: Ibid.)

Also Read: The Upcoming Economic Recession in 2017 Has Already Begun

But isn’t this the same type of insane thinking that brought about the mess to begin with? Of course it is, except instead of receiving ultra-cheap financing, you will pay banks to hold your money. Remember the days of high interest savings accounts? Negative rates will relegate them to the dustbin of history.

Even worse, most banking clients have no idea their money is at risk when held in the bank. Under Dodd-Frank Wall Street Reform and Consumer Protection Act regulations, banks can legally convert deposits to share equity during a banking crisis. It’s basically a bail-in. The bank uses your capital to plug gaping holes in their balance sheet in an attempt to stay solvent. Depositor shares may or may not be worth something down the line. But who wants to find out? How is this even morally justified?

If negative rates do come, depositors would not only be subject to holding risk, but be paying for the privilege to do so! It’s hard to imagine how Americans will agree to go along with this. It might even facilitate the banking runs regulators are trying to prevent. There’s simply no reward for holding your money in a checking account anymore.

Consequences of a Negative Rate Environment

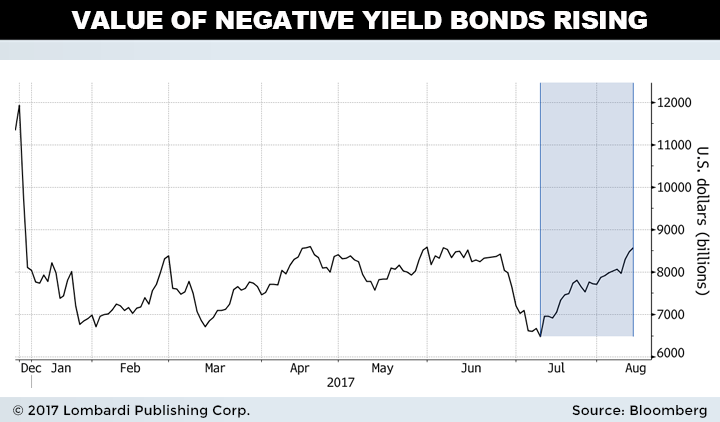

Negative rates are more common than you think. While no major American interest rate benchmark has cratered that low, credit markets in Europe have.

For example, Sweden’s Sveriges Riksbank first broke the taboo in 2009 as a response to the U.S. Housing debacle. Central banks in Denmark and Japan followed suit. The goal was to avoid a nasty recession like the one experienced in America. Those maneuvers largely succeeded, but they didn’t come without consequences.

Negative rates encourage businesses and consumers to borrow with reckless abandon. Banks, too, get charged to hold excess reserves with central banks, and this encourages excess lending and speculation. Much of the bank’s profits accrued from selling Treasury bonds back to the Federal Reserve during the Quantitative Easing (QE) program ended up in the stock markets.

From New York, Milan, Sydney, and beyond, dozens of stock market bubbles are currently raging. In America, the Cyclically Adjusted P/E ratio, or CAPE, is at the second-most expensive level in history (around 30). Most major world markets are experiencing some version of overvaluation (by varying degrees). This is all partially happening because financial institutions are re-investing excess reserves in the stock market. Just like people, they don’t earn interest income when rates are negative. It’s far more profitable to continue investing in the market, no matter how detached fundamentals get. Doubly so when there’s a great chance central banks will socialize losses when it all blows up.

Also Read: U.S. Interest Rate Prediction for 2017 Means a Return to High Stakes Risk

Another thing negative rates do is create moral hazard. In this twisted world, borrowers get paid while savers get penalized. Low interest rates already caused historic amounts of malinvestment through unproductive practices like stock buybacks and ill-conceived debt financing projects. Now, imagine how much malinvestment would transpire if borrowers were paid to take out loans on top of that. Why wouldn’t people and institutions borrow every dollar that could get their hands on? There’s no interest penalty for speculating—only principle. This would set us down a dangerous path, where the value of money is completely cheapened.

Credits: Flickr.com/401kcalculator.org

Yet one more drawback of negative rates: It becomes harder for banks to make money. We understand if no tear will be shed on their behalf. But it matters to depositors. If you recall, under Dodd-Frank, deposits are considered bank collateral and can be technically seized to prevent a bank collapse. When the banks struggle to make money, they’ll have less capital reserve on the books. Less reserve equals less ability to absorb substantial losses when the next black swan event strikes. In today’s world, the bank’s misfortune can also be your own—if they’re safeguarding your money.

That’s unless you don’t mind being a forced shareholder.

Why Would Central Banks Do It?

Negatives rates are something central banks would rather avoid. Think of them as the “nuclear option”—used as a means to an end. Since inflation has consistently failed to sustain at target levels (in America, that means two percent), negative rates are being considered as a way to force savers to spend money in the real economy. Basically, the idea is to engineer forced demand.

Some central banks use negative rates as a way of subduing currency strength. The lower the interest rate, the less incentive investors have to buy the currency. Institutional investors tend to park cash allotments into short-term currency, which pays higher interest. As many countries are actively attempting to weaken their currencies to boost domestic exports, negative rates are a useful tool.

In the end, the long-term consequences of negative rates in the real economy aren’t really known. The consequences of negative rates have have mainly affected inter-bank lending, not the mainstream consumer…yet. But when the next recession hits, Main Street might get their first taste of such a scenario.