Expect an Economic Slowdown in 2017. Here’s Why

After rising 3.5% in the third quarter of 2016, gross domestic product (GDP) in the last three months of the year slows down and rises 1.9%, an unchanged growth compared to the first estimate for January. Indeed, anyone who thought that President Donald Trump could achieve a four-percent GDP growth rate in 2017 should be prepared for disappointment.

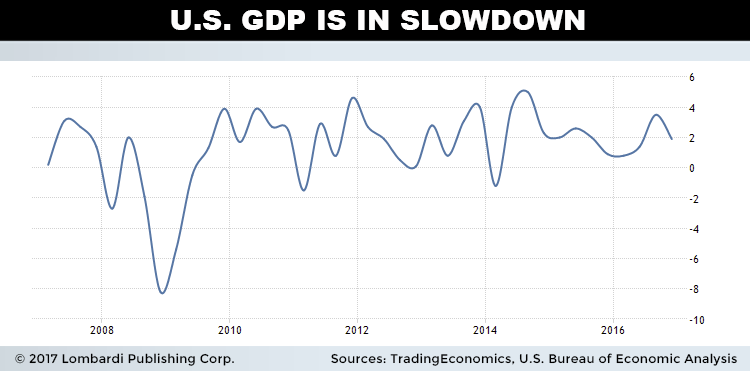

Despite the fact that taxes stunt the U.S. economic growth outlook, Americans would probably use any extra cash to reduce their debt rather than invest. It’s unrealistic to expect U.S. economic growth to speed up. Consider the chart below; the U.S. economic growth rate is brittle at best. If anything, the economy has been slowing down.

Advertisement

Indeed, there are widespread concerns about a global economic slowdown in 2017. Trump’s financial toolbox has little to offer for growth other than hope and the related tax cuts. Yet these might be implemented in 2018 at best.

What Is an Economic Slowdown?

In economics, an economic slowdown is a prelude to a recession. Though, it’s difficult to distinguish the two. Nevertheless, whereas a slowdown might not be a recession, a recession is certainly a (protracted and deep) slowdown.

An economic slowdown contrasts the idea of economic growth. Thus, it’s a condition that occurs when macroeconomic levels of production (GDP) drop below what might be achieved if all economic “inputs” available were fully exploited.

The effects of an economic slowdown become more ominous as the slowdown protracts, becoming a recession. The signs are a sharp increase in unemployment, less productivity, and a drop of consumption and access to credit. In many ways, America and much of the developed economies are still experiencing economic slowdown conditions.

Thus, nobody should dismiss the risk of an upcoming economic recession in 2017. Despite good intentions, the Trump policies might account, or even add to, the risk of slower U.S. economic growth in 2017. The problem is that Trump’s purported isolationism will only hurt the European Union’s chances of improving its own economic and social situation.

Gut instincts aren’t always right. The idea that a European Union in decline would reduce competition on the world stage for the U.S. is wrong. America both benefits and grows when European economies—and for that matter, China and Japan—are strong. However, the Trump policies will magnify the effects of the current crisis of the EU.

The Europe that is based on democratic and liberal thought, with the free exchange of goods and services, and that thrives economically, maintains a strong relationship with the United States. Conversely, the United States has reached the pinnacle of its power just as Europe was becoming more united.

Disrupt this legacy and relationship, as recommended by Trump, and both would suffer untold consequences. Such a process of disruption has already gotten underway. The old and “wholesome” American—indeed, western—values of the pursuit of happiness and prosperity, which have been the fruits of the free trade of goods and persons, have come under attack.

What Happens When an Economy Slows Down?

The enemies of these values are the very causes of the economic slowdown. They include social instability, poverty, unemployment, and new emergencies, such as terrorism and unfettered migration. These are also the effects of an economic slowdown; they simply magnify.

But the biggest enemy, still after almost 10 years, has been the 2007/2008 financial crisis. Its effects show most dramatically what happens in extended periods of low growth.

The latter has destabilized business to such an extent that no government has been able to correct, let alone identify solutions. Thus, the Trump policies have a high probability of failure as well. They may even cause more damage, because Trump’s proposed protectionism would discourage investment.

While on the subject of investment, the Donald Trump policies could hurt companies by discouraging them to look beyond the United States. They might even feel stuck in the United States, unable to thrive from areas and economic sectors of the world where demand is on the rise.

Many of the big industrial giants, even those that Trump has already “softened” into retaining major productive facilities in the U.S. like Carrier—a unit of United Technologies Corp. (NYSE:UTX)—would not appreciate import duties for what they don’t make in America. The economic advantage of the market is to produce and assemble where it sells.

Trump of all people should appreciate that markets are stronger than any artifice or mechanism to stifle them. Tariffs add to other constraints that hamper the development of many industries in the U.S. For example, many American multinationals often resort to using foreign funding.

It’s pointless to create an alternative reality. Like it or not, Americans have voted Trump into the presidency and he has a mandate to carry out his political and economic program. Still, his measures will have an impact and it’s best that investors understand what it might be in order to protect themselves.

Nobody blames voters for Trump. His victory was a natural consequence of the recent past. Thus, the new president has promised to bring America to growth rates that preceded the financial crisis of 2008. The risk is that the cure may hurt more than the disease, leaving the patient worse off. The risk is a U.S. economic collapse in 2017.

The financial crisis of 2008 was rooted in the American phenomenon of the subprime mortgage. Yet, the U.S. suffered a milder economic slowdown than the European Union and Japan. America’s problem is that it has not returned to the growth rates that the EU and Japan are accustomed to. The post-2008 recovery is the slowest that the U.S. has experienced after any recession since World War II.

Trump Faces Great Obstacles in the Effort to Make America ‘Great Again’

Trump has promised to lift the GDP growth rate to at least 3.5% or four percent against the current 2.1%. However, his recipe has failed to impress such that the U.S. GDP rate forecast for 2017 is less optimistic. As usual, economists are divided and justly so, for there are a multitude of factors and hidden risks—black swan scenarios—that could make matters worse or better.

The problem is that the recipes for growth vary sharply and even the Trump policies don’t fit entirely in the various camps. Some suggest the first thing to boost economic growth is to stimulate demand. To do that, they suggest negative interest rates. Meanwhile, rates will likely increase at least three times in 2017.

Others, meanwhile want to focus on the supply side. That means encouraging productivity by reducing regulations and strengthening investment in infrastructure and the social system. That’s Trump’s recipe and it is certainly worth encouraging. The problem is that infrastructure spending and tax cuts contradict each other.

In his economic vision, Trump has combined the two approaches. He wants to do a Captain Kirk and go where no president has gone before. Thus, he expects to inspire demand and productivity. The lower taxes plan relies on the effects this will have on businesses. The logic has no flaws, in theory.

Lower business taxes will encourage American companies to repatriate production and capital. This should allow for more spending on physical and social infrastructure. But the problem is that some American businesses are paying risible amounts of taxes, even in regions like the European Union.

Such is the need to encourage employment and investment that countries like Ireland or the Netherlands are willing to accept virtually zero income taxes from companies as rich as Google parent Alphabet Inc (NASDAQ:GOOG). (Source: “Google pays €47m in tax in Ireland on €22bn sales revenue,” The Guardian, November 4, 2016.)

Some companies might bite and take advantage of the offer. But, the nature of business and attraction comes down to incentives. The incentives may cost more than what the effort is worth.

Thus, America might grow again—and it’s already great—but it won’t grow to the extent Trump expects.

Contradictory Policies

Trump’s policies contrast one another. The lower taxes—from entities that could pay much higher ones and still remaining profitable and healthy—will not help. They will, however, contribute to bloating the already-out-of-control public debt. Meanwhile, interest rates are rising, pushing the dollar higher in a context where rival currencies like the euro are still under a zero-interest-rate regime.

Thus the U.S. economy, should it continue to grow, will not be making the leaps and bounds into a four-percent-GDP-growth territory in 2017. The best that can be expected is continued growth at the current rate for the next few months. Any Trump tax incentives won’t have any effects until 2018 is the president makes the necessary changes this year. It’s already full blown tax season in the U.S. for any 2017 effects.

Meanwhile, Trump may have made a mistake by writing off international trade agreements such as the Transatlantic Trade and Investment Partnership (TTIP) or the European Union deal. Meanwhile, the White House has even started to look for ways to reduce the scope of the North American Free Trade Agreement (NAFTA) with Canada and Mexico.

Again, as with the other policies, the goal is admirable: to bring more gains—especially jobs—but the approach might be wrong. Trump’s great skill is negotiation. He’s honed it in one of the toughest real estate markets in the world: New York City. Instead of scrapping the TPP, Trump would have done more for Americans by renegotiating it.

He could have forced a rewriting of the rules to better suit America’s role in the economy of the Asia-Pacific region. The point of contention might have been that China does not have a free-market economy, in the sense that the Chinese government offers direct ‘incentives’ or subsidies to Chinese companies.

Thus, U.S. companies don’t compete on a level playing field. Now, with fewer links to China and tenser relations, the playing field remains as slanted as ever. In this context, America may actually become weaker instead of stronger. All the while, the EU will continue to struggle, contributing little to generating demand, finding even fewer outlets beyond its borders.

The promises of the Trump election campaign, the infrastructure plan and the tax cut, for now remain on paper. Meanwhile the inevitable increased costs of borrowing could act as a brake on the GDP growth rate, which was moving rather well for a few months of 2016.