Mortgage Rate Forecast Points Higher as Fed Takes Its Foot Off Throttle

The mortgage rates forecast for August 2017 could be on the upswing, thanks to the Federal Reserve. The central bank’s plan to slowly tighten monetary conditions by gradually reducing its bond purchasing re-investments could pressure bond yields higher.

This is related to the so-called “Quantitative Tightening” (QT) that some in the media are clamoring about. It means that rates on typical 15- and 30-year mortgages should creep higher. Basically, it’s the exact opposite of the Quantitative Easing (QE) program that the Fed had in place for years after the U.S. Housing Bubble.

Advertisement

Now, the Wall Street talking heads will have you believe that bond yields are rising due to a strong economy. But that’s not the cause. After all, the peak of this growth-challenged business cycle has already been reached. If a “robust” economy couldn’t move rates sustainably higher years ago, it sure won’t be the cause of sustainably higher rates today.

Underlying the true cause of a march forward in rates is the Fed; more specifically, the Fed’s plan to start tackling its $4.5-trillion dollar balance sheet.

QE was really about money printing. The Fed would buy bonds from the big banks, who would deliver them back to the Fed and get paid money for nothing. As the Fed kept buying bonds, the constant demand would drive the long-end bond yields ever lower. It certainly isn’t “Joe Public” buying 10-year bonds with 2.3% yields (1.6% at the lows of 2016!) when core inflation is two percent. Real investors seek to make real returns.

But now that the Fed has stated its intention to whittle down its balance sheet, QE will go in reverse. Old bonds will mature, and new bonds won’t be bought. Nor will bond profits be re-invested in the marketplace. The net effect? The Fed’s balance sheet will shrink and the cost of money will increase. With more bond supply in the market, and with the Fed becoming a neutral participant, bond yields will be forced higher. Interest rates are much too low for private buyers to pick up the slack.

Expect this multiyear process to begin in September.

Are Mortgage Rates Going Up or Down?

This is the million-dollar question that homeowners would like to know. While mortgage rate predictions are never easy, they are less so today. That’s because the Fed has never been so involved in the bond market. Not so long ago, economic expectations and institutional bond demand set the course for rates. Today, not so much. The mortgage rate today is a reflection of the benchmark rate that the Fed wishes to target.

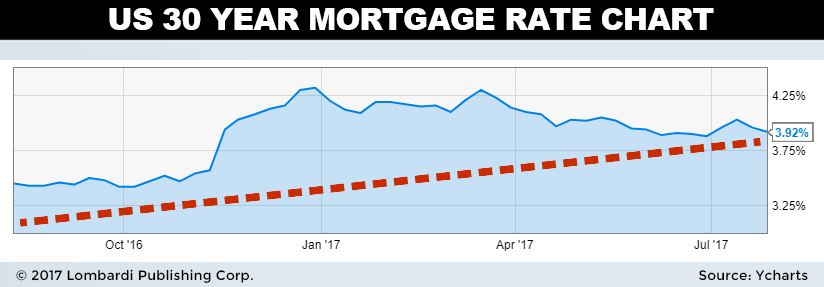

The current mortgage rate (15-year fixed) is about 3.18%, while the 30-year fixed mortgage rate is about 3.93%. Echoing expectations from Kiplinger, I expect the 15-year and 30-year fixed mortgage rate to creep higher by 20 to 30 basis points on both. This would put rates at 3.4% and 4.1% respectively. (Source: “Long Rates to Stay Low,” Kiplinger’s Personal Finance, August 1, 2017).

In other words, I wouldn’t expect upward moves in rates, but the slow creep is starting to begin. A slow creep higher in mortgage rates for August 2017 is just the start. There may be further pressure on long-end rates if the Fed raises the Feds Funds Rate (FFR) later in 2017, but that’s not a given at this point.

The key takeaway is that rates should rise, absent of non-stop Fed bond buying. Interest rate volatility could pick up when economic growth slows down to a crawl, but we’re not quite there yet. In the meantime, borrowing rates for consumer durables are on the upswing, so budget accordingly.