Global Recession Coming, Economist

The odds of global recession 2017 are building, according to some esteemed economists. For people still clinging to the idea that reflation is on the horizon, they may want to think twice. If this upcoming global recession does come, it could be on a scale unlike anything ever witnessed before.

Saxo Bank chief economist Steen Jakobsen in pinning these odds at 60% over the next 18 months, which is not what world leaders want to hear. He expects global growth to falter in the coming months as borrowing levels dominate in both China and Europe while the “Trump bump” in U.S. trading fades. This double whammy could tip the balance toward negative growth. (Source: “There’s more than 60% chance of a global recession within the next 18 months, economist says,” CNBC, April 10, 2017.)

Also Read: The Upcoming Economic Recession in 2017 Has Already Begun

In essence, Jakobsen expects the “credit impulse” in Europe and Asia to die down, which is another way of saying there’s too much debt. There’s only so much credit that can be forced into the system with budget deficits so high, so this will need to be addressed somehow. Without the gears of credit greasing the economy, stall speed and/or negative growth should stick around as far as the eye can see.

Indeed, the International Monetary Fund (IMF) has already warned of this dire over-indebtedness gripping the planet. Gross debt has more than doubled in nominal terms since 2000, and it’s still rising. Total non-financial debt sat at $152.0 trillion in 2015, which is a big problem when world gross domestic product (GDP) is only around $79.0 trillion. Slow growth is making it hard for nations to work off their debts, which is, as the IMF puts it, “Setting the stage for a vicious feedback loop in which lower growth hampers deleveraging and the debt overhang exacerbates the slowdown.” (Source: “The IMF Is Worried About the World’s $152 Trillion Debt Pile,” Bloomberg, October 5, 2016.)

China, in particular, is in rough shape. China’s debt has reached over 250% of GDP, with much of it owned by state-owned entities given the task to achieve economic growth targets at all costs. This has prompted them to borrow on thousands of large-scale infrastructure and public works projects. This would be all fine if many of these projects weren’t pork-barrel projects or zero-yielding assets. Some of these are the famous “ghost cities” that many in the financial media have been clamoring about. Overcapacity in the construction sector is rampant in China.

The other reason why China matters so much is that it is one of the select few countries who can backstop a global recession. Without China’s insatiable demand for commodities, the “Great Recession” brought about by the U.S. Housing Bubble would have been much deeper and would have lasted much longer. The People’s Republic of China is still hyper-focused on growth, but the Chinese government’s ability to answer the call is in question.

Earlier in 2017, China’s President Xi Jinping signaled that the country would no longer defend its 6.5% growth target. This is a huge deal, since China had steadfastly defended meeting ambitious growth targets in the past, much to the chagrin of economists who believed that setting growth targets would result in widespread malinvestment. They were right.

Tens of thousands of unused commercial spaces, retail stores, and residential housing litter the country. In some cases, brand new apartment complexes are demolished for the next new thing. Life cycles are measured in years, as opposed to decades. There’s even a raging skyscraper bubble; in 2016, China built more skyscrapers than the rest of the world combined. It makes the Japanese 1980s real estate bubble look like chopped liver. All this occurs as China keeps drawing down its foreign currency reserves, amounting to a dwindling supply of capital in which to ward off the inevitable hangover.

And the crazy part is, China shows no signs of slowing down. In January 2017, China racked up its biggest debt binge ever, creating $540.0 billion in new debt in that month alone. China has never gone through a recession in its first foray into capitalism, and the country’s strategy appears to be to prevent one at all costs. Because of this, at least one analyst at Deutsche Bank AG (NYSE:DB) believes that China’s debt injections will be the primary reason why the global economic boom is about to end. (Source: “China Just Created A Record $540 Billion In Debt In One Month,” Zero Hedge, February 14, 2017.)

China is just the tip of the spear when it comes to deficit spending worldwide. The reality is, all the major industrialized nations are engaging in the deadly sin. The writing is on the wall: debt saturation, both privately and publicly held, will undoubtedly yield the next global recession. Steen Jakobsen simply slapped an aggressive, but plausible, timeline on it.

Global Recession Causes & Effects

A global economic recession is a rare event. Since Word War II, only four periods (1975, 1982, 1991, and 2009) have met the IMF’s standard definition of recession, defined as “a decline in annual per‑capita real World GDP,” coupled with a decline of one or more global macroeconomic indicators. These are usually shallow affairs, lasting little more than a year before a gradual return to growth. The world economy is simply too dynamic, and forces like population growth feed a continuous pipeline of upward consumer consumption.

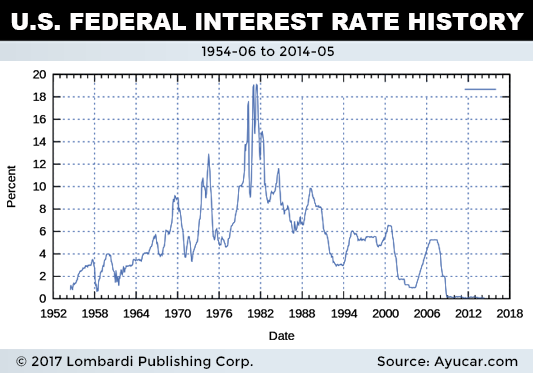

Rising interest rates in the United States have been the main factors in two previous global recessions, back when America’s influence on the global economy was much larger than it is today. The common phrase “When America sneezes, the world catches a cold” signified just how dependent the world was on American consumption, when U.S. GDP was a larger slice of the global economy. Interest rates peaked at 13% in 1974 and 20% in 1981, preluding both major recessions. Higher interest rates probably won’t be a factor this time around.

If economic growth stalls in the developed world, slowing consumption will soon affect export-dependent developing nations, dragging everyone down in the mud. This is basically how global recessions take root. Slowing consumption trickles from the top-down, until the business cycle picks back up again. Credit growth is the driver of all this, but if that threshold has been breached, there’s no equal catalyst to take its place. Credit growth is the straw that stirs the drink, and right now it’s clogged.

The effects of global recessions are quite insidious. For developed nations, unemployment becomes more prevalent. Job security declines as employers shed workers due to slack demand. Wage growth stalls due to an excess labor pool. A stock market crash may occur as corporate earnings crater and defaults rise, wiping out years of investment gains in mere months. Social problems rise, with the fringes of society turning to crime to make ends meet. All this acts as a headwind on consumer spending, akin to the snake consuming its own tail.

There are “positive” aspects to national and global recessions, however. Central banks worldwide, dominated by Keynesian ideology, tend to cut interest rates in response. This makes financing consumer durables less onerous and, quite often, interest rates stay low for a very long time. Unfortunately, this is generally in conjunction with stimulus programs (at the taxpayers’ expense), which loads even more government debt onto bloated balance sheets. This playbook has a solid history of resolving immediate crises, but does nothing to solve the actual problem. In fact, it always guarantees that the next recession will be worse.

Is There a 60% Chance of Global Recession in the Next 1.5 Years?

It’s hard to quantify the odds the same way that Saxo Bank’s sophisticated model did, but I wouldn’t argue with that assessment. There’s a host of potential negative catalysts in the world today, ranging from Trump policies to a U.S. stock market bubble to everything in between. Geopolitical risk is also at its highest point in recent memory. Populism, expressed as resistance to globalist capital structure, is threatening to roll back the movement of labor and flow of goods. This is not an ideal environment for rapid economic growth.

At minimum, a tectonic shift in the world balance of power seems likely, and this never happens peacefully. Couple all these factors with a worldwide debt bomb waiting to explode, and it’s hard to imagine how the global economy has remained so resilient for so long. Financial crisis 2017 could easily break out at a moment’s notice. Stay tuned.

In the end, the prime reason for this growing economic malaise is debt. The world is levered with debt up to its gills and, unlike in 2008, there’s no economic backstop to bail anyone out.

The U.S. Federal Reserve’s balance sheet is already packed with six times more debt than it usually holds, and the Fed is trying to unwind debt in an orderly fashion. China cannot stabilize world growth this time around, it’s facing a historic corporate debt bubble and slowing economy. The U.S. consumer is tapped out, as are consumers in most industrialized nations. The old crutch of low interest rates is no longer the silver bullet it once was, and is actually exacerbating the problem.

Why isn’t anyone solving the problem? Old central bank habits die hard I guess.