Next Recession 2019

Some analysts fear the next recession in 2019. Others warn it may have already begun and that the year for the next recession is 2018. They are both right because the economy and the markets (whose performance can trigger a downturn) are operating in a parallel universe now. Whether it’s 2019 or 2018, it seems appropriate to start asking “When will the next recession be?”

The Federal Reserve lacks a plan and it will switch to new “management” in 2018. Janet Yellen is out and Jerome Powell is in. But judging by the rumors, all of the people who will help him evaluate the best rate policy are already in disagreement. Some say there should be three rate hikes. Others fear that even two hikes might be too many. (Source: “Fed minutes show a divide over its own forecast of 3 rate hikes this year,” MarketWatch, January 3, 2018.)

Three rate hikes could interfere with plans to boost inflation to about two percent. Certainly, it could slow economic growth. Meanwhile, the interest rate policy has to confront the effects of the aggressive tax reform. Its intention is to stimulate investment and employment. But it also makes paying down the federal debt more difficult. Until recently, the U.S. dollar and its dominance of all transactions involving commodities from oil to gold have worked because of unchallenged U.S. economic and military might. Now, both those things are under threat.

What Will Cause the Next Recession?

Predicting the next recession with precision is always hard, if not impossible. But it’s even harder to pinpoint the specific cause—or causes. Only in retrospect can such a complex process as a recession be taken apart and understood. Then, there’s the fact that no recession begins the same way or under the same circumstances. For example, by any measure, most indications suggested that Donald Trump’s first year in office would have been marked by some form of economic or financial malaise.

Gold prices, after all, were going up and stocks seemed headed for a correction on November 9, 2016—the day after the 2016 presidential election. Nevertheless, perhaps unlike other recessions, there are abundant signs and hints that something isn’t quite what it seems. That something is wrong with the health of the U.S. economy. The “rules of economics” flaunting valuations on Wall Street have created the illusion of widespread prosperity. And that’s the key to guessing when the next recession is coming.

Simply, the tax reform has exacerbated the distortion in equity prices. They haven’t risen because of any organic growth—that is, from actual revenues or profits per share. They’ve risen on the expectation of profits and the fact that lower taxes will boost profits—without companies necessarily having sold more “widgets.” So far, so good. Until interest rates start moving higher, essentially offsetting the effects of the tax cuts. If borrowing costs more, even the fiscal incentives that Trump has fought to get through Congress won’t work as intended.

Uncharted Financial Territory

The United States is literally entering uncharted financial territory. Rather than help the middle and lower classes put more money in their bank accounts, fueling the economy with more spending across the board, the tax cuts have added leverage mostly to stock prices. Meanwhile, they risk pushing federal budget deficits to about $1.0 trillion.

Apart from making government shutdowns into annual events over the next few years, they fly in the face of standard practice. Now, there’s a situation where interest rates are still low but taxes are relatively lower, with plans for the government to spend to improve infrastructure. Nonetheless, it’s when the economy slows down that interest rates are low and taxes are cut. (Source: “Why the Next Recession Could Really Hurt,” Barron’s, January 23, 2018.)

The recipe for higher valuations in the stock market and higher interest rates contributes to a recession. Perhaps the recession is not an immediate one. But it could arrive by 2019 or 2020. Certainly, all the ingredients are in the cauldron and boiling. The problem is that with the low interest rates, the resulting outflow of liquidity is the reason stocks keep moving higher.

So far, the interest rate hikes have not done any damage. On the contrary, the fact that the four interest rate hikes so far that have pushed it to 1.5% after almost a decade at near zero has enhanced market performance the same way that anabolic steroids do for athletes. Investors are too confident. They have become used to picking stocks as if they were playing darts. No matter, where they land on the board, they score points.

Jerome Powell, Another Yellen

The U.S. Senate has approved Jerome Powell’s nomination to head the Federal Reserve. This allows Trump to have his cake and eat it too. After, all what’s the point of having a cake? Trump got to choose his own Fed Chair. He did so, taking care not to appoint a replacement who might tamper with Yellen’s gradual approach to rates. Trump is not shaking the boat. Clearly, he sees his legacy as one tied to stock market performance. But that’s not necessarily a good thing for the economy…or the markets.

Economy predictions for 2020, or earlier, have become uncertain at best and dire at worst. The Federal Reserve has released such an overflow of liquidity that nobody knows how equities will react in the face of the nominal rate moving to over two percent in 2018—in accordance with the course set by Yellen—and three percent in 2019.

In addition, the purpose of embarking on a course to gradually tighten the monetary supply when Yellen started to raise rates in 2015 was to avert inflation. But inflation has not come. It has not moved by much. People aren’t spending their cash. Either there’s too little of it, given few Americans have any to speak of, or they’re holding on to it because they have a pessimistic sentiment about the economy.

One of the nominees for a federal reserve seat, Marvin Goodfriend, even suggests the possibility of applying negative interest rates. This, he says, might prompt people to spend their money and fuel the inflation so many fear—even if it’s not there. (Source: “Fed nominee Goodfriend, fan of negative rates, could roil debate,” Reuters, January 23, 2018.)

Inflation Is Not Rising Fast Enough

In other words, for inflation to rise and justify the rate hikes, there needs to be actual economic growth. The kind that comes in a tide that lifts all boats. So far, there appears to be faith that this might happen thanks to the tax cuts but no evidence. The other problem about higher rates is that there’s always the risk that it may prompt investors to sell their shares. After all, the cash they earn can be put in a bank account and start to accumulate interest.

Cash, in an uncertain situation like the one higher Fed rates are creating, helps many investors deal with fear. The fear is valid. Wall Street is overvalued. The risk of an “accident” or, to use a more current term, a “black swan,” has become extremely high. Anything could burst the bubble now.

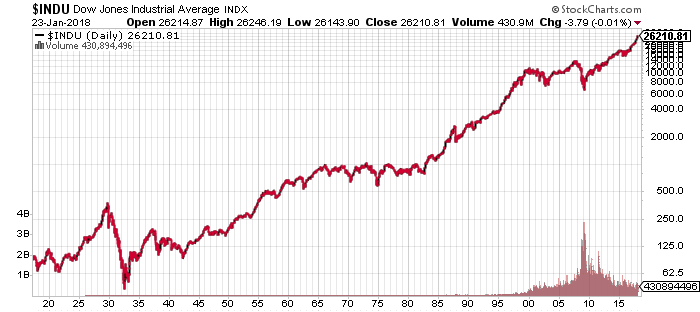

Looking at a chart of stock market performance from the last century to the present, it becomes evident that the markets have already entered a stage that finds its closest precedent in the 1990s and the dreaded October 1929 crash. Note that the latter crash was merely the earthquake that prompted the start of the equity avalanche. It would only be in 1933 that the lowest values were achieved.

Chart courtesy of StockCharts.com

Note the similarity in the way the index rose between 1923 to 1929 and 2009 to 2018. Then note the sharpness of the jagged descent from 1929 to 1933. Investors act as if drunk. They are riding the wave of euphoria and have forgotten what it’s like when they lose.

The market corrections have been minor and brief. Nobody has had the opportunity to burn their fingers and many investors have never known what it’s like to confront a bear market or the kinds of interest rates that were once considered normal. As recently as the early 2000s, rates were in the order of seven to nine percent. That would be positively catastrophic today.

The Trump tax plan is a convenient way to mask deeper problems in the American economy. The cuts didn’t just materialize from thin air. The government will have to find the funds to keep the many services that Americans need—including very rich Americans. Evidently, medical services will suffer. The much-lauded infrastructure schemes may start. But there’s a risk the government will run out. Borrowing, meanwhile, will become more expensive, adding billions to the interest payments on the federal debt alone. Individual families, meanwhile, will face higher interest on mortgages and loans. Oh, by the way, it was higher interest rates that caused the real estate bubble to explode in 2007-2008.

Rather, Trump should have pushed for tax cuts. But the bulk of the benefits would have been better “invested” in the middle and lower classes. That would truly have increased spending. It would also have helped debt repayment, reducing risk. Instead, for most people, the tax breaks are almost insignificant and they’re not guaranteed to last.

Perhaps, had Trump persisted in conducting an isolationist foreign policy, he could have made some concessions by cutting military spending. But this too is different. There are risks of wars in Asia and the Middle East and Trump seems ready to go in with both feet and all fleets. Somewhere, sometime, someone will have to pay the bill.