Overvalued Stocks Could Trigger 2017 Stock Market Crash

Stocks don’t crash because they are fairly valued. The stock market crashes when investors realize that stocks are significantly overvalued and are either spooked or lose patience. And, right now, we are in the most overvalued stock market ever.

Stocks are more overvalued in 2017 than in 2000, 2007, and even 1929. Investors looking for a spark to trigger the upcoming stock market crash don’t need to look any further than rising geopolitical tensions and/or the raft of underwhelming U.S. economic data rolling in.

Whether stocks are overvalued is not even in question any more. They are. It is to be expected on some levels. After all, the current bull market is in its ninth year and is the second-longest on record. It makes sense that the S&P 500 would be overvalued to some degree.

It just doesn’t make sense that stocks are this significantly overvalued. Especially when you consider that the current economic expansion has been the slowest since World War II. Yet still, here we are, after years of artificially low interest rates and financial engineering, stock valuations are, according to all major key indicators, at or near their highest levels ever.

The S&P 500 is less than two percent below the March 1, 2017 all-time high, and the S&P 500 price-to-earnings ratio is at more than 24 times earnings; the highest multiple in almost 15 years. (Source: “P/Es & Yields on Major Indexes,” The Wall Street Journal, last accessed April 21, 2017.)

These current levels are unsustainable, and many experts predict a stock market crash. Dr. Marc Faber maintains that stocks are overbought and that investor sentiment is too bullish. The markets will eventually reach a tipping point that will trigger massive selling that will be like “an avalanche.” (Source: When selling starts in markets, it’ll trigger an ‘avalanche,’ Marc Faber says,” CNBC, February 26, 2017.)

George Soros, the founder of the $4.5 billion Soros Fund Management LLC and the 23rd wealthiest person in the world, said, “Right now uncertainty is at a peak. And, actually, uncertainty is the enemy of long-term investment. So I don’t think the markets are going to do very well.” (Source: “Soros Says Markets to Slump With Trump, EU Faces Disintegration,” Bloomberg, January 19, 2017.)

Billionaire investor Paul Tudor Jones said stocks are bloated to levels not seen since 2000, just before the NASDAQ plunged 75%. He also noted that the value of the stock market relative to the size of the economy should terrify Janet Yellen. (Source: “Paul Tudor Jones Says U.S. Stocks Should ‘Terrify’ Janet Yellen,” Bloomberg, April 20, 2017.)

Scott Minerd at Guggenheim Partners said he expects a “significant correction” this summer or early fall. Philip Yang at Willowbridge Associates predicts that the stock market will spiral down between 20% and 40%. Meanwhile, BlackRock, Inc.’s perma-bull Larry Fink thinks that stocks could fall up to 10% if first-quarter earnings are disappointing.

2017 Stock Market Crash in the Crosshairs

These stock market predictions for 2017 are dire. But they are well founded. The stock market is going to crash, like it always has, because valuations are in nosebleed territory and eventually, investors will pay attention to fundamentals and cease paying as much attention to momentum and technicals.

Boom will turn to bust. It’s a natural cycle that the stock market goes through and, every time it has crashed, the market has rebounded and moved on to record levels. Right now though, the big question is: how big will the stock market bubble get before it bursts?

For now, chances are excellent that the stock bull market will continue. Well, there’s little to fuel the current bull market right now, but investors want to see something more concrete. Optimism is so high right now about Donald Trump and his pro-growth “America First” policies that they are willing to give him some time to prove that his pro-business policies will actually boost corporate profits and juice the U.S. economy.

Unfortunately, the U.S. economic outlook for 2017 does not look good. This does not bode well for the long-in-the-tooth bull market.

On the campaign trail, Donald Trump basically said that U.S. gross domestic product (GDP) had been pathetic under President Barack Obama. For starters, Obama is the only president to never have realized a single year of at least three percent GDP growth. Under Obama, GDP growth averaged just two percent. In 2016, Obama’s last full year of office, U.S. GDP growth was just 1.6%.it

Trump said he wants to get annual U.S. GDP back to the good old days of four percent. To do that, he wants to slash taxes, cut red tape, and increase spending. All of which will make it easier for corporate America to compete, which will, accordingly, jolt the U.S. economy and put more money into the pockets of the average American.

But it looks like the anemic growth under Obama is going to follow Trump for a little while. We’re almost 100 days into the Trump presidency and all the economic data points to a slowdown.

Underwhelming U.S. Economic Data Pushes Stocks Higher

For starters, the U.S. economy added fewer jobs than expected in March; just 98,000 versus the projected 180,000. This is also 55% fewer jobs than the 219,000 created in February. Yes, the unemployment rate fell to 4.5%, but the underemployment rate is near nine percent. The labor force is flat at 63%. (Source: “Employment Situation Summary,” Bureau of Labor Statistics, April 7, 2017.)

Consumer confidence may be at a 17-year high but that doesn’t mean Americans are confident enough to actually spend. Consumers are optimistic about the outlook for jobs and wages…not the here and now. Not surprisingly, U.S. retail sales fell in March for the second month in a row. (Source: “Advance Monthly Sales for Retail and Food Services,” United States Census Bureau, March 2017.)

It’s tough for the vanishing middle class to consume the U.S. economy to four percent GDP when nothing is changing as far as the economy goes. Jobs are aplenty, but most of the jobs created during the so-called economic recovery have been low-paying part-time jobs that offer little-to-no security or wage growth.

To help survive the economic recovery that most people do not even know we are in, U.S. households have piled on debt that is approaching pre-Great Recession levels, and will set new records later this year.

In the fourth quarter of 2016, household debt was at $12.6 trillion. The previous record was in the third quarter of 2008, when household debt was at $12.7 trillion. Over the last 10 years, household debt has soared 11% to an average $132,529.(Source: “Household Debt Increases Substantially, Approaching Previous Peak,” Federal Reserve Bank of New York, February 16, 2017.)

For now, delinquency rates are low, but that will change when massive high-interest debt collides with rising interest rates. How do we know? Half of all Americans (47%) already say they would have to borrow money to come up with an emergency expense of $400.00. (Source: “66 million Americans have no emergency savings,” CNBC, June 21, 2016.)

All of this is bad news for a country that gets more than 70% of its GDP from consumer spending. And is it any wonder that the current economic expansion is the slowest since World War II?

What about Trump’s planned tax cuts and increased spending? That’s still on the table, but what it will actually look like is open for debate. Trump had to shelve his American Health Care Act (AHCA) because the bill didn’t have enough votes to pass.

If Trump can’t get something passed that was supposed to be an easy victory, what are the chances he can get his other campaign promises passed as originally touted? The odds of Trump being able, even in a best-case scenario, to get U.S. GDP to four percent will be virtually impossible.

This will lead to decreased revenue and earnings and will gut consumer confidence, which could lead to a stock market sell-off and eventually, a stock market crash.

3 Key Indicators Say Stock Market Is Significantly Overvalued

The stock market is only as strong as the stocks that make it up. And, right now, the stock market is done partying like the Wall Street crash of 1929; euphoric investors have moved on to trying to out-party the tech bubble of 2000.

But just how big is the stock market bubble? Three of the leading stock market valuation ratios point to the stock market being significantly overvalued. The markets have only been higher once, and that didn’t end well.

According to the Case Shiller cyclically adjusted price-to-earnings ratio (CAPE) ratio, the S&P 500 is overvalued by more than 80%. The CAPE ratio compares current prices to average earnings over the last 10 years. The ratio is currently at 28.85; the long-term average is 16. That means, for every $1.00 of earnings that a company makes, investors are willing to pay $28.85. The CAPE ratio has only been higher twice: in 1929, it was at 30 and in 1999, it was at 45.

(Source: “Online Data Robert Shiller,” Yale University, last accessed April 21, 2017.)

Warren Buffett might not be telling anyone that the stock market is overvalued, but his favorite indicator is.

The market-cap-to-GDP ratio is referred to as the Warren Buffett Indicator because Buffett believes “it is probably the best single measure of where valuations stand at any given moment.” (Source: “Warren Buffett on the Stock Market,” Fortune, December 10, 2001.)

The market-cap-to-GDP ratio, which compares the total price of all publicly traded companies to GDP, is at 129.6%. A reading of 100% suggests that stocks are fairly valued. The ratio has only been higher once since 1950. During the dotcom bubble in 1999, it was at an eye watering 153.6%.

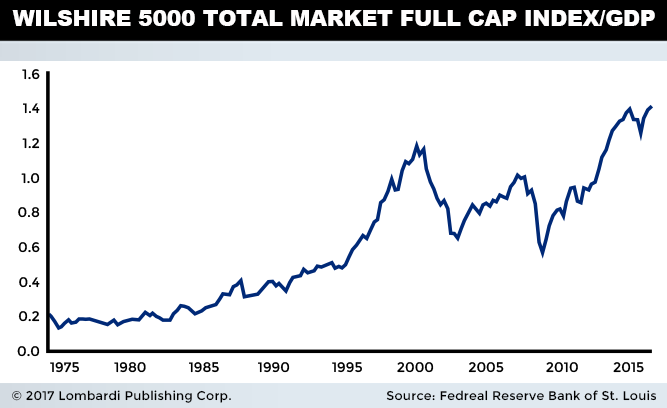

The Wilshire 5000 to GDP ratio is a market cap-weighted index of all actively traded U.S.-headquartered stocks that trade on the major exchanges. The Wiltshire is less well known than the CAPE ratio and the market-cap-to-GDP ratio, but it is actually the largest index by market value in the world. The ratio is at an all-time high of 140.5. (Source: “Wilshire 5000 Total Market Full Cap Index/Gross Domestic Product,” Federal Reserve Bank of St. Louis, last accessed April 21, 2017.)

How Far Could Stocks Fall in a 2017 Crash?

How far could the markets fall when the stock market does crash?

- 1929: Wall Street crashed on Black Tuesday (October 29, 1929), sparking the most famous bear market in history. The S&P 500 fell 86% over the next three years and did not surpass its previous peak until 1954.

On Black Tuesday, the Dow Jones Industrial Average (DJIA) fell 18.5% in intra-day trading to 213, before closing the day at 230, for a one day loss of 11.7%. In July 1932, the DJIA hit an all-time low of 40.54, which is a three-year collapse of approximately 86%. It took more than 25 years for the DJIA to recover.

- 2000/2002: The dotcom bubble burst in March 2000. Over the next two years, the NASDAQ collapsed, losing close to 80% of its value. The S&P 500 fell approximately 50%.

- 2007/2009: The housing bubble burst in 2007 and stocks started to sell off. By March 2009, the S&P 500 lost 56% of its value, while the Dow collapsed 54%.

- 2017/2018: The markets are as overvalued as they were in 1929 and have room to run, which would put them closer to the 2000 dotcom crash. At current levels, a 1929-type stock market crash would put the S&P 500 near 300, levels not seen since 1988. To match a dotcom-type meltdown, the S&P 500 would have to crater to around 1,100, erasing six years of gains.

A similar Great Depression-type stock market crash in the Dow Jones forecast for 2017 would put the index at around 2,880, levels last seen in early 1991.

Financially Engineered Stock Bull Market

The broader indices are at record levels, not because of a long history of strong revenue and earnings growth. In fact, the S&P 500 just emerged from a record long earnings recession. Not that investors cared; they still sent the S&P 500 regardless.

Nope, the S&P 500 and DJIA are at unsustainably high levels because of artificially low interest rates and financial engineering. Artificially low interest rates were supposed to make it easy to borrow and spend. All it really did, if weak GDP data and other economic indicators have any merit, is gut retirement portfolios. Income-starved investors were forced to take their money from safer investments (bonds, CDs, Treasuries) and put it into riskier investments like the stock market.

Wall Street, knowing that the U.S. economy was doing poorly, financially engineered their books and propped up weak earnings by initiating aggressive share buyback programs. During the so-called economic recovery, buyback programs helped propel the S&P 500 into record territory. Roughly 30% of the increase in the S&P 500 between the third quarter of 2009 and the end of 2016 was a result of share repurchase programs.

That trick is coming to an end. Rising interest rates in the U.S. mean that fewer companies will be able to borrow cheap money to buy back shares, prop up their share price, and pay out frothy dividends.

Again, investors can only be distracted for so long. Eventually, they will stop chasing momentum and pay attention to fundamentals like valuation. It happened in 2000 and it will happen again. And, like the dotcom bubble, the sell-off will start slowly, then gain steam.

In March 2000, the tech bubble peaked and the selling started. No one knows why the dotcom bubble topped out in March 2000 or why the sell-off started when it did. It just happened. There was no warning. Investors just started to dump tech stocks with unsustainable and totally unjustifiable valuations. Analysts said it was just some profit taking, then it was a slight correction, then it was a bloodbath.

The stock market is overvalued and it will follow the same path as the other stock market bubbles before. I don’t know when it will start, but the warning signs are there. I do know though how it will end.