The Silver Forecast for Q1 2018

The silver price forecast for the next three months is bullish. The political and economic uncertainties leading to a stock market that’s out of control, bold corporate tax cuts, and American and international political turmoil have confounded investment strategies in 2017. The remarkable—and remarkably odd—ride that cryptocurrencies have had, however, may have created the proverbial “disturbance in the Force.”

Distractions and Disturbances in the Force

Cryptocurrencies have distracted those investors who, in search of alternatives to overvalued stocks and a stock market on steroids, want alternatives. But many should have known better. Cryptocurrencies are, at best, unproven entities. The crypto party may already have entered the hangover phase, despite the efforts of some to defend their Bitcoins and Ethereums. Those who survive with their appetite for investment intact may consider revisiting the classics like gold or silver in 2018.

Advertisement

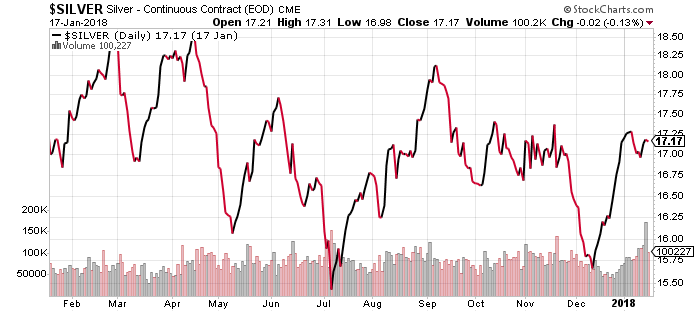

The market chaos may already be upon us. That’s why the silver price forecast for Q1 2018 demands your attention. The next few months could see a major shift. Noted global bank HSBC Holdings plc (LON:HSBA) expects silver to be one of the sleeper hits of 2018. It says the silver price per ounce should hover around $17.20. (Source: “New Risks Could ‘Spark’ Demand For Silver In 2018 – HSBC,” Kitco Metals Inc., January 16, 2018.)

The silver price today was $17.02.

Silver price predictions rely on a similar logic to what moves gold. Thus, as gold prices are also showing signs of a reawakening, silver should follow in step. Moreover, silver relies even more on industrial activity and demand for metals in general. The expectations are that metals, in general, will become more valuable in 2018, given rising global industrial production.

The United States saw gross domestic product (GDP) increase steadily in 2017. Europe and Japan are starting to register higher-than-expected growth rates as well. Car sales, for instance, have not been this high since the period before the 2008 financial crisis. North America witnessed a similar trend beginning about two years ago. (Source: “European car sales at highest level in 10 years,” ABC News, January 17, 2018.)

Perception vs. Reality of Growth

Growth and the perception of a stronger economy may fertilize the financial markets, but menacing clouds of risk are approaching and could rain on the stock parade. President Trump’s honeymoon period is over. He’s about to start his second year in the White House. Rather than giving up, his critics are getting louder.

Special Prosecutor Robert Mueller continues to harp on about the Russiagate investigation, as fruitless as it has been, trying to find even the smallest element to build a solid case. So far, he’s missed the mark, but the distraction of close Trump associates like Steve Bannon being subpoenaed damages confidence. In other words, the prospect of impeachment continues to dangle over Trump’s head.

The only policy area where Trump has been able to build bipartisan consensus is the Middle East. Trump appears to have made a complete turnaround on his 2016 campaign promises of staying away from international crises. Instead, he’s allowing them to ferment. His Jerusalem decision has already sparked violence, increasing tensions between Israel and its neighbors.

It’s Back to 2016 and Unpredictability

Trump seems to be looking for the kind of tension that could prompt U.S. intervention. For example, Trump’s secretary of state, Rex Tillerson appears to have signaled a major shift in Trump’s policy toward President Asad in Syria. There are credible musings of a deployment of some 30,000 U.S. troops at the border between Syria and Turkey now. Meanwhile, even as North and South Korea are working toward patching up their differences, deciding to march together at the Olympics games (to be held in Pyeongchang in February), the White House continues to escalate preparations for some kind of an intervention.

In other words, U.S. foreign policy has become more unpredictable while doubts linger as to whether Trump will be able to finish his term in office or be forced to resign. As long as the U.S. remains the world’s leading superpower, its policies and international actions play the biggest role in determining the kind of political risk that affects markets. Middle Eastern oil producers tried to corrupt that pattern in the 1970s. But their influence has waned.

Given that nothing has changed in Trump’s presidency from the moment after the election—and that the risks associated with it have increased—a referral to the metals and commodities market in November 2016 is useful.

Silver—and gold—achieved its highest peaks in the summer of 2016 when Trump was confirmed as the Republican nominee. It peaked again in November with his presidential win. In 2017, silver achieved its highest valuations in March/April, when it seemed that Trump could challenge Russian interests in Syria.

Silver Price Chart

Chart courtesy of StockCharts.com

Thus, we should expect the price of silver and gold to rise significantly. They could go much higher than analysts have predicted, because of the multiple uncertainties. Global markets—but Wall Street, in particular—are sustaining an excessively bullish cycle. The tax cuts have prolonged it. But if those tax cuts do not result in actual growth, all that will be left is the mountain of federal debt and fewer tools to confront it.

The debt risk limits the Federal Reserve’s ability to raise rates. Many expect more rate hikes in 2018. But doing so risks making the federal debt problem much bigger. It could also compromise the purchasing power of average Americans, bursting the auto loan and housing bubbles. While the market optimism continues, the silver price per ounce should rise or hold around the present $17.00-18.00 level. But as the economic and monetary realities of the tax reform—combined with all the risks—materialize, the silver spot price could go much higher.