Financial Deregulation Is a Recipe for Another Credit Crisis in 2017

Last month, President Donald Trump issued two decrees that could cause a credit crisis in 2017. Trump may have raised the specter of global financial collapse. The new president wants to repeal, or resign to insignificance, the rules that President Barack Obama used to keep banks’ speculative urges in check.

It’s not clear to what extent the economy has been recovering. The numbers fail to render an accurate picture. But, at least in theory, the regulations have probably helped prevent a global financial system collapse. Indeed, the sub-prime crisis that broke out in 2007 has only gone in occultation. Its effects could strike back at any moment.

Advertisement

All it would take to trigger the banking crisis and financial erosion back to life is the possibility to take more risk. President Trump will have achieved just that by lifting the Dodd–Frank Wall Street Reform and Consumer Protection Act and its Volcker Rule. These have acted as barriers on speculative activity. The unraveling of these rules imposed on banks after the 2008 crisis has raised fears of a return to the old bad ways.

Thus, Trump has recreated the very conditions that were in place before the crisis. Predictably, central bankers such as European Central Bank (ECB) President Mario Draghi and U.S. Federal Reserve Chair Janet Yellen have expressed alarm over this. As he had promised, Trump began to deregulate the U.S. economy, to the great satisfaction of Wall Street.

The satisfaction of Wall Street might translate to a kind of risk inebriation. What’s good for Wall Street has proven, on too many occasions, not to be good for Main Street. As the Dow Jones flirts with 22,000, it becomes harder to believe, but the chances of a U.S. stock market crash in 2017 have gone up.

The regulatory atmosphere is such that the markets have become more vulnerable to a crash. The Republican Party strongly criticized Obama’s restrictions on the markets. In effect, the markets have had to strengthen their ability to avoid bankruptcy while testing their ability to absorb economic upheavals.

But, just as Democrats are criticizing everything Trump does now, Republicans criticized Obama’s initiative even when it served the overall health of the capitalist system well. Obama, and many free-market pundits, realized that often the markets need protection from themselves.

Left to their own devices, the markets would take on excessive levels of risk, remaining vulnerable to small and large shocks alike. The risk is that, to keep up, the European banking system might also pursue more deregulation, raising its own susceptibility to risks. The thing about risks is that they can often be triggered by events nobody expected.

Trump’s financial deregulation has actually prompted a more pessimistic U.S. economic outlook for 2017. Financial deregulation is dangerous. By pursuing it, Trump has inadvertently set the stage for the next crisis. Specifically, the deregulation measures will allow banks to take risks with loans again.

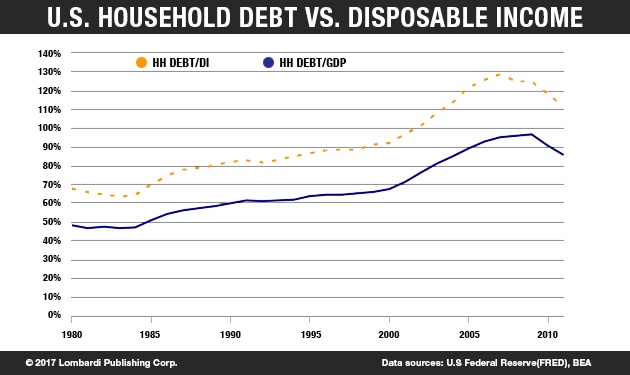

Consider the incredible level of U.S. household debt (and disposable income), much of it accumulated before the 2007 crisis. Another major banking crisis would exacerbate this situation.

The lifting of the Dodd–Frank Act would allow banks to get back into the mortgage game in a big way. But, by doing so, the banks will demand protections and rules about the ability to repay loans. They could resume the practices that allowed the sub-prime crisis to mushroom. Deregulation would also allow banks to become over-indebted again.

What Is a Credit Crisis?

In other words, Trump’s proposed deregulation has raised the possibility of a new banking crisis. But what is a banking crisis? A banking crisis is a situation in which banks find it difficult or impossible to repay creditors. That is, they do not have the liquidity to do so immediately. They usually get into such situations from having made bad investments that have lost their liquidity.

Monetary and financial authorities try to resolve, or prevent, such situations by imposing regulations such as Dodd-Frank. Without such rules, there is a risk of a credit crisis. A banking crisis inevitably produces a credit crunch or a credit crisis. This can occur as banks are forced to tighten credit by reducing the general availability of credit (as a form of protection).

It usually also involves tightening the conditions required for the granting of loans, i.e. credit. A credit crisis necessarily implies that lenders have entered a situation of mistrust of the markets, whether out of their own doing—as in 2007—or other factors. Regardless of the source of the problem, they are often associated with financial or economic tensions and collapse.

Trump’s deregulated banks, moreover, might find it hard to draw any benefits in the context of tighter import controls. In other words, Trump’s policy is schizophrenic in the same way that Obama’s foreign policy vis-à-vis Syria was. Trump desires ultra-libertarian regulatory conditions for banks while imposing the tightest tariff regime in decades.

The tight tariffs mean that many U.S. industrial groups will be forced to absorb higher production costs. In the case of General Motors Company (NYSE:GM) or Ford Motor Company (NYSE:F), for example, they will be forced or encouraged to produce in Ohio or Michigan rather than Mexico. Yet, Mexico might be much cheaper.

Trump’s deregulation proposal is not new of course. It’s part of the free-market ideal to believe that deregulation benefits the rich as well as the poor (trickle-down economics, anyone)? During the election campaign, as Trump was trumpeting his recipes to boost the economy, his Democratic Party critics conveniently forgot a significant tidbit about banking deregulation.

It was the Bill Clinton administration that pushed through financial deregulation in the 1990s. There are short memories on Capitol Hill. President Clinton repealed the Glass-Steagall Act. He removed this obstacle for big capital to maneuver in the markets. But, at the time, the markets were performing in a spectacular way.

The Glass-Steagall Act, part of F.D. Roosevelt’s New Deal, dating back to 1933, separated commercial banks and investment banks. This was done to protect the real economy, investors like you and me, from financial ventures and financial vultures. Clinton “modernized” the act.

This allowed institutional investors, pension funds, insurance companies, commercial banks, and investment banks to integrate the functions that Roosevelt separated.

Thus, Congress and voters were more than happy to let that pass. The same might be said about the present situation. The markets appear to be pursuing their natural course toward moving higher. Dips are always temporary, but some have long-lasting effects. The 1929 crash led to a decade of economic depression around the world.

That depression might even be cited as one of the causes of World War II. The 2007 crash led to a recession that, it turns out, may have actually been a depression. Its effects linger worldwide. The fact that inflation has struggled to increase—statistically at least—has shown just how hard the economic recovery has been.

The global economy is still reeling under the effects of the post-2007 banking crisis and financial collapse. The reason is that banks simply stop lending, preventing economic growth. That happens to be one of Trump’s major complaints. His prescription to resolve the credit crisis, however, could end up adding to the problem. Moreover, there are derivatives to confront.

Derivatives were not as prominent in the Bill Clinton years as they were in the G.W. Bush and Obama years. But, if there’s something that responsible investors have learned after the 2007 financial collapse, it’s that derivatives are the financial equivalent of sharks in the ocean.

Could Derivatives Be the Causes of the Credit Crisis?

Derivatives are second-tier financial “products” or instruments. They get their name because they are related, that is they derive from another financial product. They are risk on risk. But, in theory their value depends on the product to which they are related. This could take the form of a bond or a stock or, better yet, an option. They could even be related to a future or commodity.

Regardless of the type, derivatives have become a trademark instrument of high-risk funds. These are the rather ironically named “hedge funds.” They operate under the notion of engaging with the market to produce the highest possible return while protecting themselves against bad investments.

The derivative represents a bet between two parties on the future value of the product to which they are related. That’s what makes it such a risky financial instrument. As in any good challenge between two parties, a third party is the necessary loser, who takes the hit. In 2007, the losers were investors everywhere—except those who got out in time, thanks to alert hedge fund managers, as depicted in the Hollywood Movie The Big Short.

But derivatives have extended their levels of “relationship.” There are derivatives derived from other derivatives. Such products and their proliferation have made the markets weaker. They have added an extra dimension of “gambling.” Yes, there are gains for a few lucky winners. But many will lose.

Regulations like Dodd-Frank were adopted to reduce the level of risk posed by derivatives or similar high risk-investing. The market’s so-called ability to regulate itself is rather mythical. Markets are the sum total of the actions of regular human beings. Thus, they reflect their collective wisdom, not that of a would-be financial Yoda.

Derivatives were one of the main triggers of the subprime crisis in the United States. It led to the collapse of Lehman Brothers Holdings Inc., one of the leading U.S. investment banks, and destabilized the international financial system. It sent banks into crisis mode and we are still feeling the effects of the credit crisis.

Conversely, Donald Trump’s deregulation plan goes against the very people who voted for him. Deregulation favors the very elites that Trump accused during his campaign. The big banks, the elites, cheered Trump’s plans to repeal Dodd-Frank. That should raise people’s concerns.

For the time being, Trump’s changes will concern the United States. But this will eventually affect the international banking system. The European banks have no plans, for now, to repeal regulations. To facilitate cross-border banking exchanges, someone will have to give up something.

Meanwhile, the global credit crisis continues. The banks still face bad loans worth billions of dollars. The effects of the credit crisis have been a sharp reduction in production, trade, and consumption. This has put many businesses on their knees. Many have failed for not being able to pay employees and previously obtained loans.

The high risk of Trump’s financial deregulation would worsen the effects of the global credit crisis and raise the risk of economic collapse in 2017.